We use cookies where necessary to allow us to understand how people interact with our website and content, so that we can continue to improve our service.

We only ever receive anonymous information, and cannot track you across other websites. View our privacy policy

21.06.2026

Beyond the EU reset: how to supercharge the UK economy

BEST FOR BRITAIN asked Frontier Economics to independently model the economic effects of potential scenarios for UK-EU integration.

MODELLING EU-UK INTEGRATION SCENARIOS AND THE EFFECTS OF PROTECTIONISM

BEST FOR BRITAIN asked Frontier Economics to independently model the economic effects of potential scenarios for UK-EU integration.

Foreword

Tom Brufatto

Executive Director of Policy and Research

The Starmer Government has sown the seeds of opportunity, by successfully resetting our relationship with the EU after years of acrimony. Negotiations on a food and drink deal, an emissions trading deal and a Youth Experience Scheme are set to conclude soon.

With annual UK-EU Summits planned, there has been much speculation about what may come next. The political uncertainty engulfing the government will undoubtedly have momentarily tempered expectations, but the economic reality and choices ahead will remain unchanged.

As such, this independent report by Frontier Economics, commissioned by Best for Britain, will serve as a guide for the economic growth that is on offer across some of the available options for a UK-EU relationship, by modelling different levels of trade integration between our economies.

The results demonstrate how our prosperity is intrinsically tied to the EU. Beyond the UK-EU relationship reset, all further integration brings economic benefits. Any further distancing from the EU – as suggested by Nigel Farage – would bring further economic hardship.

But along the path to further integration, the choices Starmer and future Prime Ministers make will have drastically different outcomes on our economic fortunes. The EU has ruled out any further ‘cherrypicking’, which likely means the government’s options will start to narrow to the available options for integration: a bespoke UK-EU Customs Union; seeking to join the EU Single Market; or applying for full membership of the EU.

The report allows us to give conservative estimates of the growth on offer from these more ambitious models. However, some of those options come with unsavoury trade-offs.

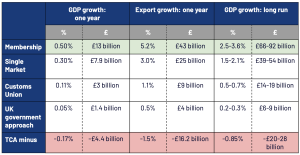

For example, a bespoke UK-EU Customs Union would provide 0.5%-0.7% of long run GDP growth. But in return for a £14-£19 billion economic boost, a Prime Minister would cede control of at least part of our trade and tariff policy, with little to no say on how such decisions get taken. We would also have to have some difficult conversations with those countries with which we have signed trade deals since leaving the EU.

Further integration with (including membership of) the EU Single Market would provide a more substantial long-run GDP boost of 1.5%-2.1%. While voters would be more likely to feel the £39-£54 billion uplift to the UK economy, they might also find the compromises involved even less palatable than a Customs Union scenario. It would require the UK to become a ‘rule taker’, with limited say over the regulations affecting most of the UK economy – an unprecedented and unsuitable decision for a leading G7 economy.

Instead, membership of the EU would have a truly transformative effect on the UK economy. By modelling the key benefits of membership – namely, closer integration into the EU Single Market and deeper integration on goods trade associated with a Customs Union – we see long term growth estimates of at least 2.5%-3.6%.

The £66-£92 billion boon would recoup at least 90% of the economic hit we took as a consequence of leaving the EU. It would deliver at least six times more growth than all the UK’s post-Brexit trade deals combined, and 24 times the GDP growth of our trade deal with India.

Perhaps most importantly, membership of the EU would distribute the proceeds across the UK. The modelling suggests that, as well as London, growth would be felt most strongly in the East and West Midlands, Yorkshire and the North East. Due to an outsized boost to trade in goods, Britain’s former industrial and manufacturing heartlands stand to gain the most. One year on from the government’s Industrial Strategy, it is clear that EU membership is an essential step to making ‘reindustrialisation’ a reality.

Membership of the EU is not without political complexity. However, comments from Michel Barnier last week suggest that it would be ‘perfectly possible’ for the UK to have carve-outs again on the Euro, or the Schengen travel area. Of course, it would require a future Prime Minister to negotiate our budgetary contributions to the EU. But of all the options available, it is the only one that would give the UK decision-making rights, putting us in control of trade policy and the rules affecting our economy.

Ten years on from the Brexit referendum, as negotiators put the final touches on the agreements from last year’s summit, this report gives an idea of the potential economic benefits of the options that lay ahead. The conclusion couldn’t be clearer. To truly transform the UK economy, we must have a conversation about membership of the EU.

The options

Best for Britain asked Frontier Economics to model five scenarios:

-

-

-

Scenario 1: Closer integration through an agreement on Sanitary and Phyto Sanitary Measures (SPS). This captures a substantial proportion of the benefits associated with the UK government’s current approach.

-

Scenario 2: Deeper regulatory alignment on goods and services. This captures a substantial proportion of the benefits of the Single Market.

-

Scenario 3: More liberal rules of origin between the UK and EU. This is one way of assessing goods trade integration of the type associated with moves towards a Customs Union.

-

Scenario 4: A combination of deep goods and services alignment with liberalised rules of origin. This captures a substantial proportion of the benefits associated with EU membership.

-

Scenario 5: Greater regulatory distance, and increased trade friction. This reflects a scenario where the UK loosens trade ties with the EU, away from the TCA baseline.

-

-

Best for Britain also asked Frontier Economics to layer the potential impacts of US tariffs onto Scenarios 4 and 5.

Frontier Economics used a ‘New Quantitative Trade Model’, which defines tariffs and alignment as changes to trade costs, applied to a baseline to give impacts in different scenarios. The model estimates changes in trade, output, welfare and prices, based on assumed changes to tariff and non-tariff barriers.

The results below are a conservative guide to the effects of each scenario. By modelling a substantial proportion (but not all) of the benefits of each option, they represent a lower limit of the growth on offer through deeper integration.

For example, the modelling for the current government approach does not estimate the impact of the emissions trading or electricity agreements currently being negotiated. Similarly, the Single Market and Membership models do not assess the economic implications of freedom of movement. In addition, evidence shows that the decision to leave the EU and the uncertainty around the future UK-EU relationship dampened investment in the UK. It is possible that commitments for further integration could positively impact investment.

Modest estimate of EU membership benefits

The report’s findings suggest that EU membership could grow UK GDP by at least 2.5-3.6% in the long run, boosting the economy by at least £92 billion.

Membership could therefore recover 90% of the OBR’s estimated 4% hit to UK GDP as a result of Brexit.

The benefits of the Membership scenario are greater than the sum of the Customs Union and Single Market scenarios combined, demonstrating the positive interactions between the reforms in removing barriers to trade.

The short-term effects of the Membership scenario are also significant, increasing GDP by 0.5% (or £13 billion) in a year.

In a Membership scenario, regional benefits are relatively evenly spread. The regions that benefit the most strongly, relative to the UK government’s current approach, are the West Midlands (0.53% increase in Gross Value Added), Yorkshire (0.47%), and the East Midlands (0.47%).

This is because of the importance of goods trade to those regions, particularly in sectors that are sensitive to changes in rules of origin. These regions therefore benefit from scenarios that reduce trade costs in industrial goods. For example, 73% of the West Midlands’ exports were in transport and machinery, where there are strong automotive and aerospace sectors.

1 / 4

The GDP benefits of EU membership far eclipse the benefits of the UK’s post-Brexit trade deals. UK government estimates suggest a combined £15 billion long-term GDP boost from FTAs agreed since the UK left the EU: Japan, Australia, New Zealand, Comprehensive and Progressive Agreement for Trans-Pacific Partnership (a bloc covering 11 other countries), India, and the Gulf Cooperation Council (six Middle Eastern countries).

By delivering a £92 billion GDP boost, EU membership could be worth at least 6 times this combined amount.

An EU Membership scenario would also deliver substantial benefits for the EU and its Member States. In the long run, the EU could see GDP growth of 0.3-0.4%.

Further divergence

Both the Conservative Party and Reform UK have opposed the government’s EU reset. Conservative Leader Kemi Badenoch called it a step backwards, criticised ‘dynamic alignment’ as making the UK a ‘rule taker’. Reform Leader Nigel Farage went further by promising to ‘scrap’ the May 2025 Summit commitments entirely.

Reversing the reset would, at minimum, return the UK to TCA-only arrangements. But ties could weaken further, for example through regulatory divergence. This could happen passively (where the EU updates rules and the UK does not follow) or actively (where the UK chooses to set different rules). Divergence would increase trade costs and could, in sensitive areas where the EU expresses disagreement, trigger retaliatory measures or a suspension of the TCA (for example, if level playing field commitments were breached).

Separately, the Conservatives and Reform UK have also pledged to withdraw from the European Convention on Human Rights, which could lead the EU to suspend the TCA in whole or in part.

To capture these scenarios of weaker trade ties, the modelling estimates the economic impacts of greater regulatory distance and further trade frictions. In reality, should the TCA be suspended entirely, these effects would be more severe.

Loosening ties with the EU could reduce UK GDP by 0.5 to 0.8% in the long-run, leading to a £28 billion hit to the economy. For the EU, the hit to GDP could also be significant (a 0.1% decrease, equating to $28 billion in monetary terms).

US tariffs

Frontier Economics have also modelled scenarios where the United States levies tariffs on the UK and other trade partners. This demonstrates the extent to which each of the five different models of UK-EU integration might shield both parties from the effects of US tariffs.

Frontier Economics modelled a scenario where the US imposes a 10% tariff on all partners except China, who are modelled as facing a tariff of 30%. The aim being to establish a baseline to compare the effects of the integration scenarios in a world of more volatile US trade policy, rather than to reflect current US policy specifically.

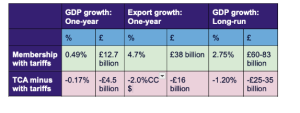

In such a scenario, UK GDP still increases by 2.3-3.3%. UK global exports would still increase by £38 billion.

The EU is more exposed to US tariffs than the UK. The US is a larger partner to the EU than the UK, with trade shocks therefore having a greater impact. Services are also a larger share of the UK’s exports than they are for the EU, which shields the UK from some of the worst effects.

Nevertheless, deeper integration with the UK shields the EU from the worst impacts of US tariffs. Comparing the difference that arises from the EU in a membership vs TCA minus scenario, with US tariffs overlaid, we see a gain of around $116 billion. This suggests that for the EU, deeper integration with the UK is a robust mitigation strategy in a world of US tariffs.

1 / 2

Modest estimate of the benefits of a Customs Union

A Customs Union scenario could grow UK GDP by 0.5-0.8%. One-year growth in exports would be around £9 billion, driven almost entirely by growth in industrial goods exports. There is a modest negative effect on services trade, because trade costs on UK-EU trade in goods have fallen, but have remained unchanged for services. Goods-intensive regions such as the West Midlands would benefit the most (though four times less than they would should the UK rejoin the EU).

The modelling suggests that a Customs Union scenario would recover only 15% of the OBR’s estimated 4% hit to UK GDP as a result of Brexit. Full membership of the EU could be worth at least five times more.

Modelling less stringent rules of origin is one way of assessing deeper integration of the type associated with moves to a Customs Union. However, it is unclear what a bespoke UK-EU Customs Union would look like. Trade costs would decrease further through the removal of customs checks and rules of origin compliance requirements. However, the UK would need to accept trade and tariff policy being set in Brussels, and it is unclear what would happen to the UK’s post-Brexit trade agreements.

Modest estimate of Single Market benefits

A Single Market scenario could grow UK GDP by 1.5-2.1%. One-year growth in the UK’s global exports would be around £7.9 billion, with the highest gains in industrial goods but also strong gains in services.

The modelling suggests that a Single Market scenario would recover around half of the OBR’s estimated 4% hit to UK GDP as a result of Brexit.

By modelling a comprehensive approach to mutual recognition and a commitment to minimise regulatory divergence, the model captures key elements of single market integration in goods and services. However, single market participation would in reality require accepting freedom of movement (not modelled here, given it is outside the trade cost framework). It would also require a significant amount of ‘rule-taking’ from Brussels on most areas of regulation, with the UK participating in decision-shaping forums but without the full decision-making rights that come from EU membership.

Sign up for our newsletter

Get our research, campaigns, and analysis in your inbox. No spin, no noise — just the evidence-led case for a better Britain.